Confused by your options with the enrollment period looming? Here’s how to pick the perfect provider for you

During open enrollment season, you need to crunch numbers, assess coverage choices, and above all, make sure you pick a plan that fits the needs (and budget) of you and your family.

That’s a tall order! After all, the young, single college graduate just joining the workforce has different needs than a two-income family of four. From single parents to 50-something empty nesters and all points in between, we each have our own health care decisions to carefully weigh.

No sweat—just take our lead and use this handy three-step guide to sort through the numerous health plan options.

STEP 1: ASSESS YOUR NEEDS

Before you can shop wisely, you need to take a quick self-assessment. Answer the following questions:

• Who do I need to cover? Is it just me, a spouse, or a whole family?

• What’s my monthly budget for premiums and out-of-pocket costs?

• Can I cover my deductible in an emergency?

• Do I (we) use health insurance rarely, occasionally, or a lot?

• Is there a favorite doctor who must be covered on the plan? (Don’t forget any specialists, ob-gyn’s, chiropractors, counseling and alternative medicine.)

• Am I offered coverage through my employer? Or will I be shopping for insurance directly through a provider or on an Affordable Care Act (ACA) exchange?

STEP 2: KNOW YOUR OPTIONS

Now you’re ready to sort through the various healthcare options, listed here in relative order from lower to higher monthly premiums:

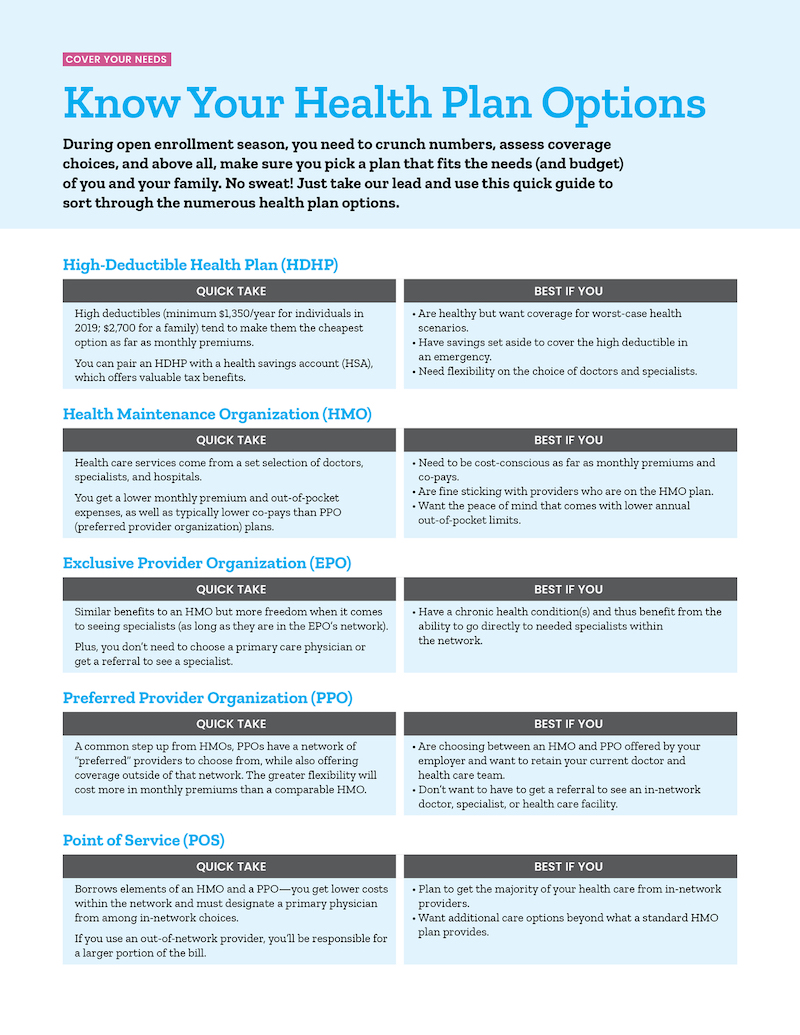

High-Deductible Health Plan (HDHP)

Quick Take: To qualify as an HDHP under IRS rules as of 2019, the deductible must be $1,350 annually at a minimum for individuals, and $2,700 for a family, with a maximum out-of-pocket limit of $6,750 for individuals and $13,500 for families. For 2020, the deductible must be at least $1,400 for individuals; $2,800 for a family. And the total yearly out-of-pocket expenses can’t be more than $6,900 or $13,800, respectively.

Main Advantage: This tends to be the cheapest option as far as monthly premiums. Perhaps more importantly, you can pair an HDHP with a health savings account (HSA), which offers some valuable tax benefits and allows you to roll-over the funds from year to year.

Main Disadvantage: Those high deductibles can be a major financial burden for families who don’t have enough funds socked away in an HSA to cover routine and unexpected medical expenses. That means all doctor and specialist visits are on you until you’ve met that annual out-of-pocket threshold.

Best for Someone Who:

• Is generally healthy and doesn’t anticipate having a lot of health care needs, but wants to be sure they're covered in worst-case health scenarios.

• Has savings set aside to cover the high deductible in an emergency.

• Needs flexibility on the choice of doctors and specialists.

• Wants to accelerate their retirement savings by taking advantage of the tax advantages of an HSA.

Health Maintenance Organization (HMO)

Quick Take: In this common set-up, you get all of your health care services from a limited selection of doctors, specialists and hospitals.

Main Advantage: The HMO negotiates contracts within its network for discounted rates, and it generally doesn’t cover any health care expenses outside of that network. Thanks to the lid on costs, you get a lower monthly premium and out-of-pocket expenses, as well as typically lower co-pays than with PPO (preferred provider organization) plans (which are explained below).

Main Disadvantage: If your preferred doctor or specialist is not a part of the HMO network, you’re out of luck. You’ll also need to go to your primary care physician for any referrals to specialists.

Best for Someone Who:

• Has to be cost-conscious as far as monthly premiums and co-pays.

• Is fine sticking with providers who are on the HMO plan.

• Doesn’t have a lot of savings set aside and wants the peace of mind that comes with lower annual out-of-pocket limits.

Exclusive Provider Organization (EPO)

Quick Take: In this setup, you have similar benefits to an HMO but more freedom when it comes to seeing specialists (as long as they are in the EPO’s network).

Main Advantage: The service fees tend to be lower than what are available in PPO plans (which are explained next), and you don’t need to choose a primary care physician or get a referral to make an appointment with a specialist.

Main Disadvantage: Outside providers are not covered (except in cases of emergency—you’ll need to refer to individual plans for its specific limitations).

Best for Someone Who:

• Has chronic health conditions and thus benefits from the ability to go directly to needed specialists within the network.

Preferred Provider Organization (PPO)

Quick Take: A PPO is a common step up from an HMO, giving insured members a network of “preferred” providers to choose from, while also offering coverage outside of that network but at a higher cost.

Main Advantage: You get to keep your existing doctor and specialist, even if they aren’t in the PPO network.

Main Disadvantage: A PPO will cost more in monthly premiums than a comparable HMO.

Best for Someone Who:

• Is choosing between an HMO and PPO offered by their employer and wants to retain their current doctor and health care team.

• Doesn’t want to have to get a referral to see an in-network doctor, specialist or health care facility.

Point of Service (POS)

Quick Take: This plan borrows elements of an HMO and a PPO. You get lower costs within the network and must designate a primary physician from among in-network choices, but your insurance will cover providers outside of it.

Main Advantage: Flexibility—you get the advantage of saving costs by using in-network health care services, while also being able to go to any doctor or specialist should you want to go to one outside of the network.

Main Disadvantage: If you use an out-of-network provider, you’ll be responsible for a larger portion of the bill.

Best for Someone Who:

• Plans to get the majority of their health care from in-network providers, and only rarely or occasionally from outside of it.

• Wants additional care options beyond what a standard HMO plan provides.

Membership and/or Concierge Medicine

Quick Take: In these relatively new setups, you pay a monthly or annual fee to have unlimited access to your primary care physician or group practice (plus any specialists and labs that they may have partnered with), saving insurance for hospitalizations or surgeries.

Main Advantage: You establish a closer relationship with your doctor and don’t put off going for small complaints that might otherwise turn into something more serious.

Main Disadvantage: Nothing is covered outside of the membership doctor or organization you’ve joined.

Best for Someone Who:

• Wants a close relationship with their primary care physician.

• Is in good health and can buy a high-deductible, low- premium policy for use in emergencies.

• Has savings set aside to cover other out-of-pocket costs that may arise.

STEP 3: PICK YOUR PLAN

Ready to enroll? If you’re going through your employer, you’ll need to talk to human resources regarding the next open enrollment period (generally November through mid-December). If you’re shopping for health care on your own, you can go directly to providers to shop their plans, shop an aggregation site like ehealthinsurance.com, or go to your state’s ACA exchange through healthcare.gov. The open enrollment period for ACA plans for 2020, which have a start date of Jan. 1, runs from Nov. 1 to Dec. 15, 2019.